2025Q1 Credit Monitor: Where Balance Sheets Weakened

Our latest Credit Monitor reviews first quarter financial trends across ~750 corporate North American bond issuers, focusing on the evolution of two key metrics: leverage and interest coverage. This update evaluates changes over both the most recent quarter and the past year, providing a view on changes to corporate balance sheet health.

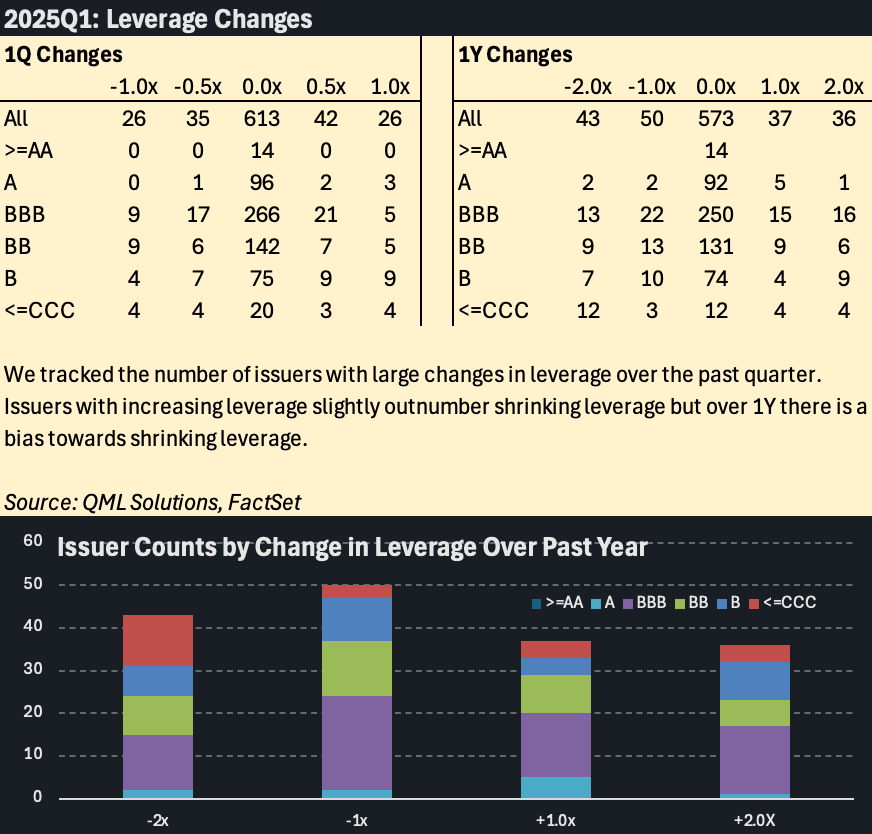

Leverage Trends

Leverage, measured as gross debt-to-EBITDA, showed a relatively balanced distribution across issuers:

61 issuers experienced a decrease in leverage of more than 0.5 turns over the prior quarter, while 68 issuers saw leverage increase by the same amount.

Over a one-year horizon, 93 issuers reported a decrease of more than 1 turn, and 73 issuers experienced a rise in leverage exceeding 1 turn.

These changes reflect a tug-of-war between improved earnings at some companies and rising debt burdens at others.

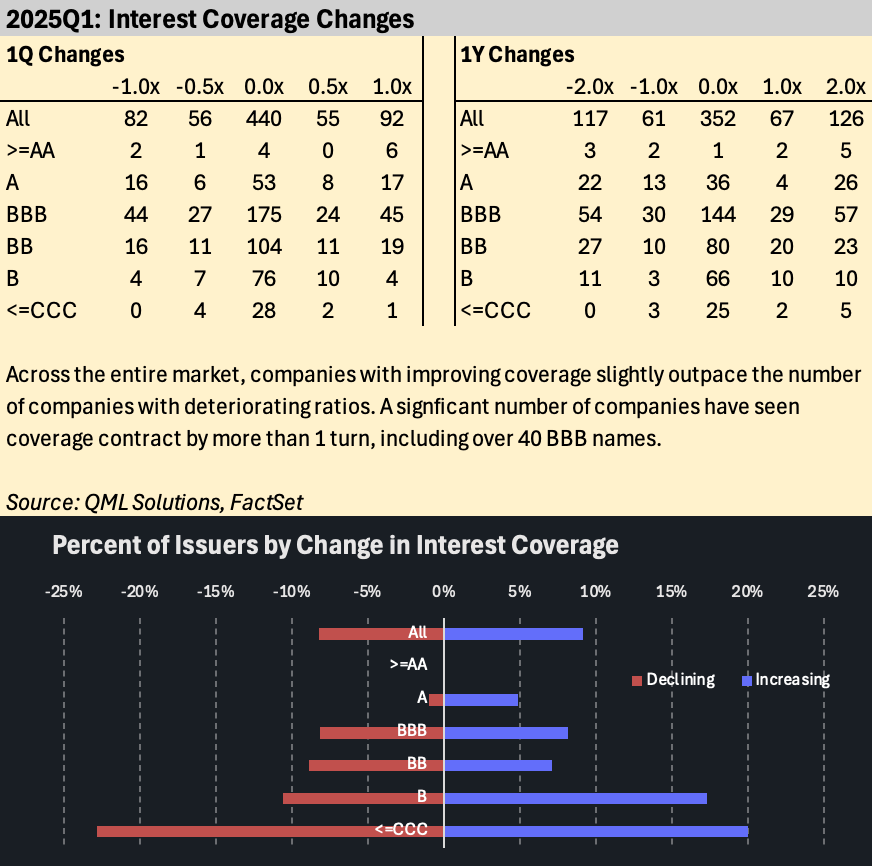

Interest Coverage Trends

Interest coverage—defined as EBITDA divided by interest expense—also showed a bifurcated pattern:

Over the past quarter, 138 issuers saw coverage decline by more than 0.5 turns, while 147 issuers reported an improvement of that magnitude.

Over the past year, 117 issuers experienced a decline of more than 1 turn, whereas 193 issuers saw coverage improve by over 1 turn.

These shifts were influenced both by the trajectory of corporate earnings and the impact of higher borrowing costs as older debt matures and is refinanced at elevated rates.

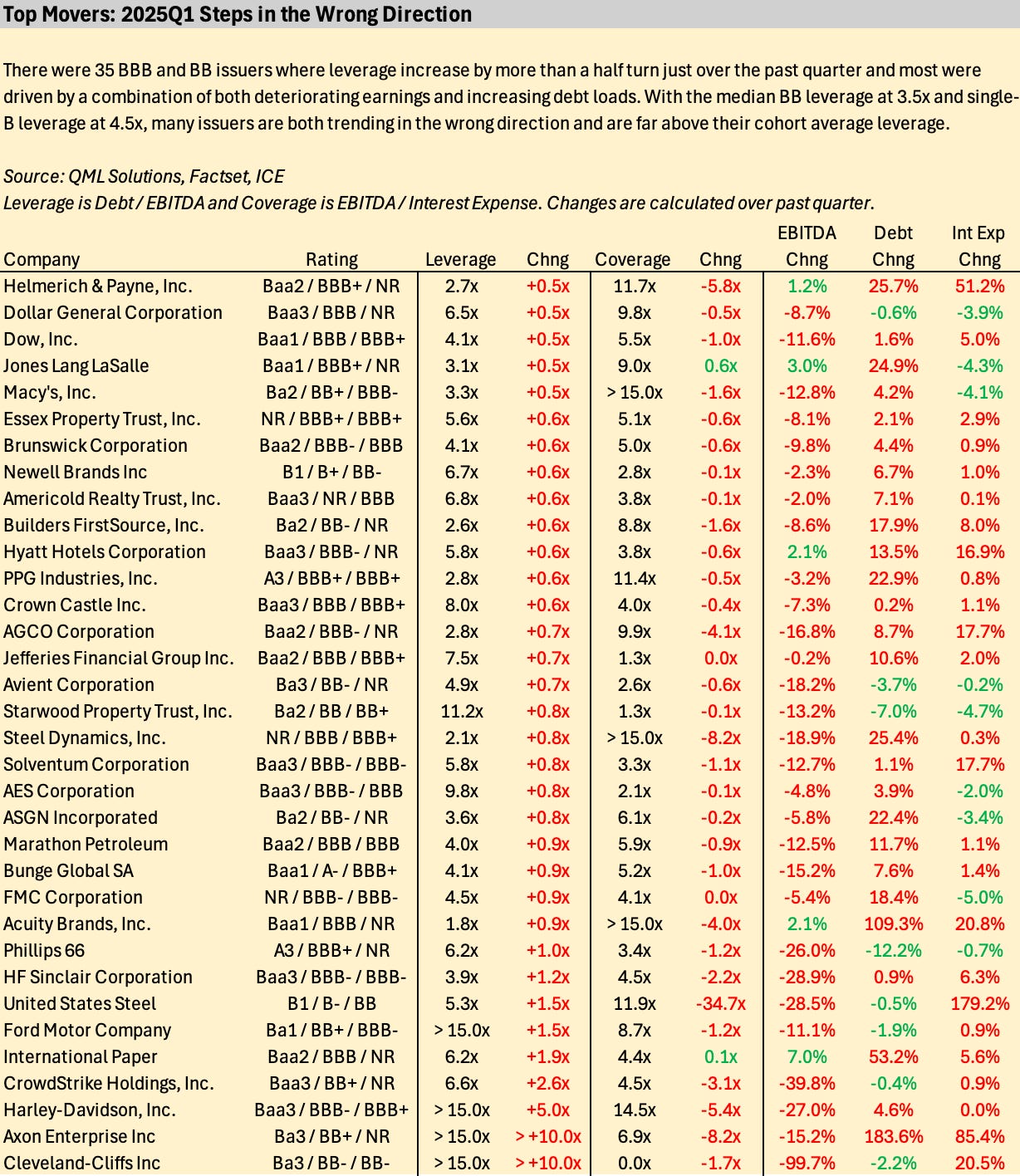

Spotlight on Deteriorating Issuers

While the overall market appears balanced, a notable subset of issuers showed broad-based credit deterioration this quarter. The table below highlights BBB and BB-rated companies that experienced a leverage increase of more than 0.5 turns over the past quarter. Importantly, many of these issuers also reported declines in interest coverage, signaling weakening fundamentals across multiple dimensions of credit quality.

In most cases, the deterioration to credit quality was driven by the multipronged deterioration of falling EBITDA, increased debt balances, and rising interest expense. These factors suggest mounting credit risk even prior to the more recent ramp up in recession risk.

By sector, Basic Industry contributed the most deteriorating names, with eight issuers, followed by Real Estate with five and Energy with four. Of the total, 25 companies were rated BBB and 10 were rated BB, underscoring that even within investment grade, financial pressure is building for select issuers.

The content published by QML Solutions is for informational and educational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security or financial instrument. The views expressed are solely those of the authors and are subject to change without notice. While we strive for accuracy, we make no guarantees about the completeness or reliability of any information presented.Any investment decisions should be made in consultation with a qualified financial advisor and based on your own objectives, financial situation, and risk tolerance. QML Solutions and its authors disclaim any liability for any direct or consequential loss arising from reliance on the information provided.