Corporate Credit Spreads: Thin Risk Premiums Leave Little Cushion

The low spread market is not the same as a low risk environment.

Investors dipping into lower ratings are receiving far less compensation than average, with many risk premiums below median historical levels.

After adjusting for duration, the incremental risk premium between BBB and BB is just 87 bps — near historic lows.

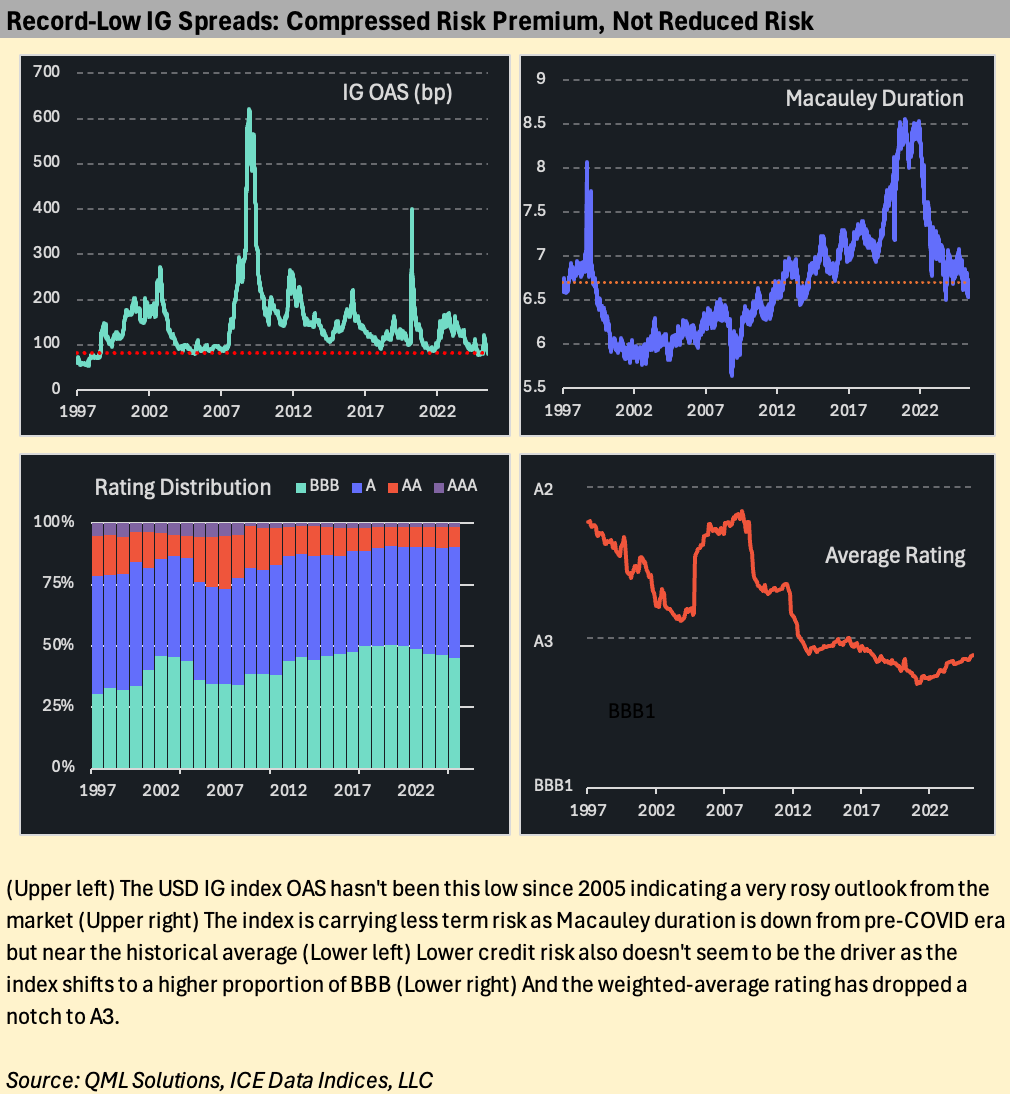

The Investment Grade (IG) corporate bond index option-adjusted spread (OAS) fell to 80 basis points last week, down about 10 basis points from a month ago. This marks the lowest IG spread level since 2005, an extraordinary milestone after nearly two decades of market and macroeconomic shifts.

It may just be sentiment—or “vibes”—but this hardly feels like the lowest-risk environment in 20 years. Markets appear to have fully discounted potential negative policy from Washington, and inflation or stagflation concerns are now firmly in the rearview mirror. Yet corporate and economic fundamentals don’t seem strong enough to justify spreads this tight, especially with the index skewing toward lower-rated BBB and medium-duration bonds.

If underlying credit risk isn’t materially lower than in past cycles, the implication is clear: today’s ultra-tight spreads reflect a compressed risk premium. At 80 basis points, the IG risk premium sits in the 7th percentile of its distribution over the past 28 years—meaning investors are being compensated less generously than almost any other time.

While the tilt toward lower ratings and medium duration does not fully explain the unusually low risk premium at the index level, ratings remain a key driver of OAS differentials within the corporate asset class. Ratings explain much of the variation in OAS across individual bonds, making it important to measure and understand these rating-based risk premiums properly.

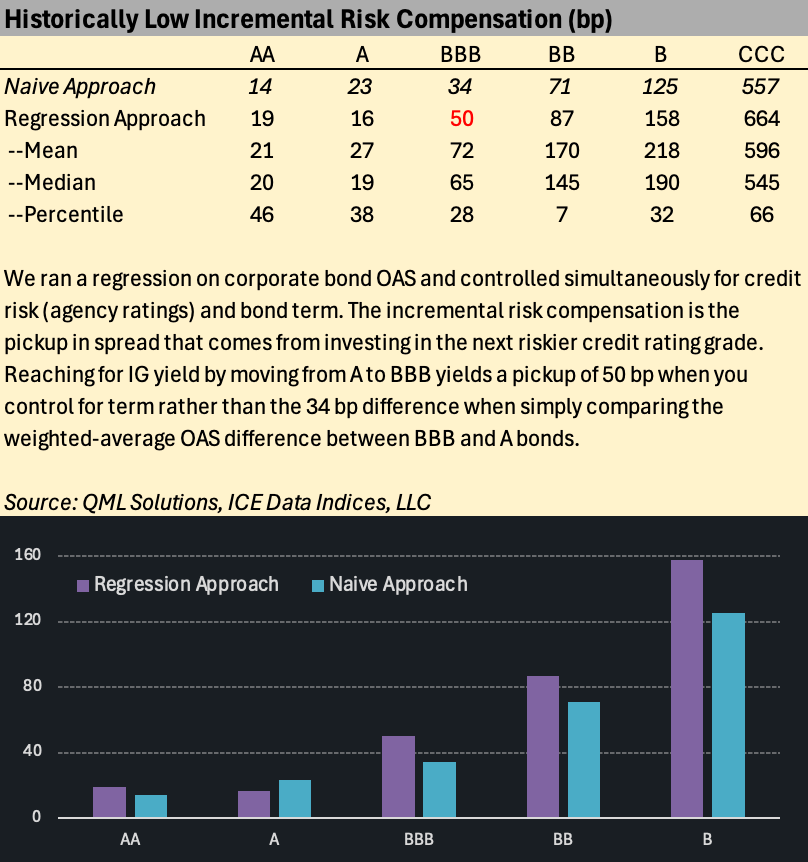

A common—but misleading—approach is to simply compare average OAS by rating bucket. For example, while BB bonds currently trade 71 bp wider than BBB bonds, they also have an average duration roughly 2.5 years shorter, which works in the opposite direction, confounding the pure credit effect.

To control for such effects, we regressed OAS on both rating and term across the ICE USD corporate bond index, isolating the incremental spread premium attributable to rating alone. This adjustment generally increases the estimated risk premiums:

The IG/HY (BBB → BB) premium rises from 71 bp (simple average) to about 87 bp after adjusting for duration.

Within IG, moving from AAA to AA earns about 19 bp, from AA to A another 16 bp, and from A to BBB about 50 bp.

Within HY, stepping from BB to B adds roughly 158 bp, and dropping further to CCC earns about 557 bp.

We can also assess how attractive these risk premiums are relative to history. For instance, the 50 bp pickup for moving from single-A to BBB-rated bonds is well below the long-run average of about 72 bp and the median of 65 bp, placing today’s BBB premium in the 28th percentile of its historical range.

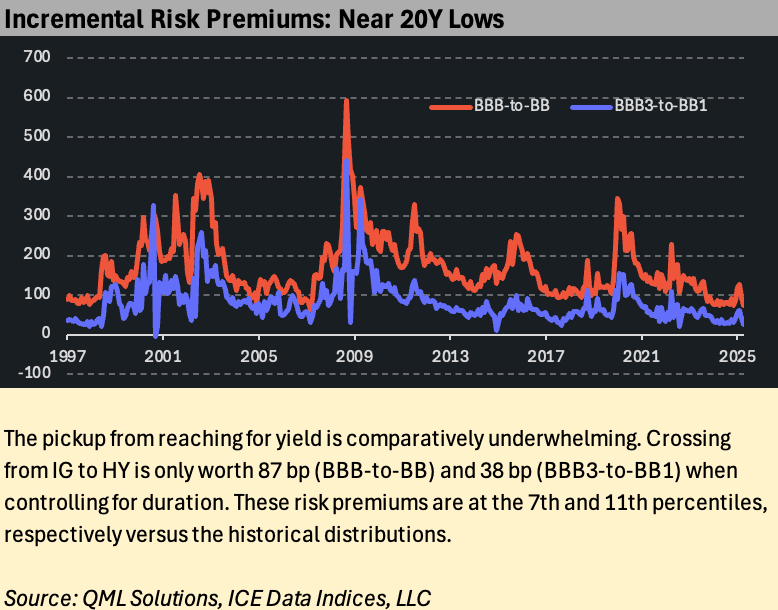

Most rating tiers today offer below-median risk premiums, with the IG/HY boundary particularly compressed. The 87 bp spread pickup between BB and BBB sits in the 7th percentile, near the narrowest premium since 2005. A more granular look shows the premium between BB1 and BBB3 at just 37 bp, in the 11th percentile of its historical distribution. In other words, investors reaching down the credit scale for yield are being paid far less than history suggests is typical.

The content published by QML Solutions is for informational and educational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security or financial instrument. The views expressed are solely those of the authors and are subject to change without notice. While we strive for accuracy, we make no guarantees about the completeness or reliability of any information presented.Any investment decisions should be made in consultation with a qualified financial advisor and based on your own objectives, financial situation, and risk tolerance. QML Solutions and its authors disclaim any liability for any direct or consequential loss arising from reliance on the information provided.