Credit-Equity Convergence Part 1: The Rise of Correlation

The first in our series of articles reveals how the co-movement of stock and bond indices has ramped up in recent years.

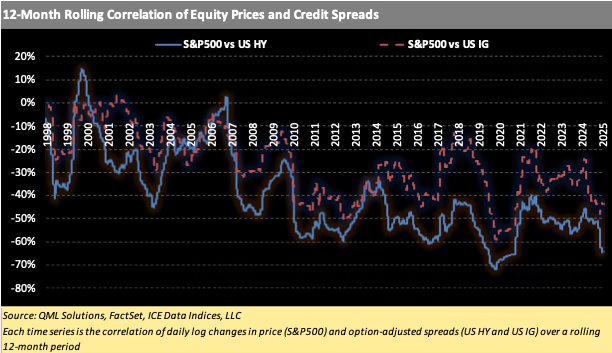

Credit spreads and equities are increasingly inversely linked. The correlation between S&P 500 price returns and US HY/IG spreads has reached -50% to -60%, levels approaching those seen during the COVID shock.

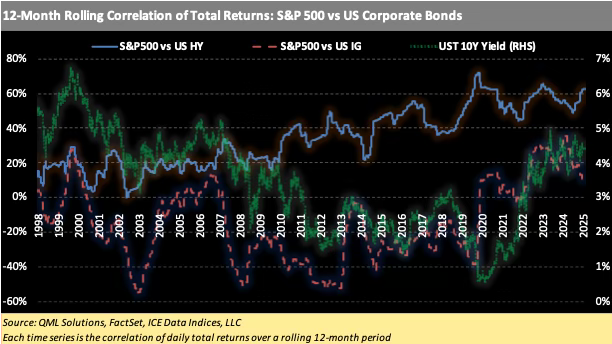

Equity and credit returns are moving together more than ever. The correlation between S&P 500 and US High Yield total returns has risen from near zero in the early 2000s to over 60% today.

Equity is now amplifying moves in credit. The beta of S&P 500 to US HY total returns recently hit 3.5, signaling that equity market performance is increasingly sensitive to credit risk sentiment.

As credit behaves more like equity, the separation between income and growth assets is eroding, reshaping how investors need to approach portfolio diversification.

Introduction

The risk and return profile of corporate bonds lies on a spectrum between sovereign bonds and equities. Investment grade (IG) bonds are closer to sovereign debt, while high yield (HY) bonds behave more like equities. The two asset classes developed along very different lines, with relatively illiquid credit providing income and highly liquid stocks providing growth. Today, the distinction between credit and equity is becoming increasingly blurred, and nowhere is that more evident than in the rising co-movement between major equity and credit indices.

In this series, we explore how and why credit markets are beginning to behave more like equities. This first installment focuses on the statistics: the correlations, betas, and risk sensitivities that increasingly link equity and credit markets.

Stocks and Spreads – Inverse Correlation Deepens

Over the past two decades, the correlation between S&P 500 price returns and HY or IG option-adjusted spreads (OAS) has grown steadily more negative. In simple terms, when stocks rise, spreads tighten, and this relationship has never been stronger.

During the early 2000s, the equity/spread correlation was noisy and inconsistent. But in recent years, it has become persistently negative, reaching -50% to -60% in 2025, levels previously only seen during the COVID crisis.

Total Returns – Credit and Equity Move in Sync

It’s not just spreads. Total returns across equities and credit have become more correlated, particularly between equities and high yield:

In the early 2000s, the correlation between S&P 500 and US HY total returns hovered around 0 to 20%.

Since 2020 correlation has remained well above 40%, and in 2025 it rose above 60%, a level exceeded only by the onset of the COVID pandemic.

For most of the past 25 years, investment grade returns were inversely correlated with stock returns, providing significant diversification benefit. Since 2022, however, the correlation between S&P 500 and US IG total returns has turned positive, and is now consistently around +15% to +25%. As shown in the chart below, rising rates is one driver of the increased correlation between stocks and bonds, which can be expected to persist in a “higher for longer” scenario.

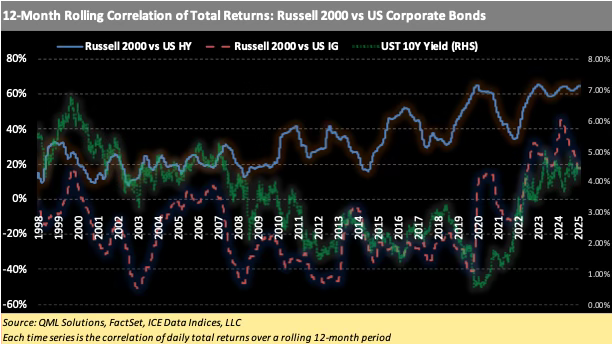

The Russell 2000, a broader and more cyclically sensitive equity index, shows a very similar pattern. Its total return correlation with both IG and HY credit has trended upward in the past five years.

One of the more striking developments is that the beta of S&P 500 returns to US HY returns recently reached an all-time high of over 3.5. For every 1% move in US HY total return, the S&P 500 has moved more than 3.5%. This is not credit following equity, but rather credit amplifying equity. In a world where credit increasingly trades like equity, this is an example of the equity market behaving like a leveraged expression of credit conditions. Credit might be expected to lag equities, but today it often leads, particularly in capital markets dominated by central bank policy, liquidity flows, and ETF behavior.

What’s Next – The Drivers of Convergence

In future reports in this series, we’ll take a look at the structural forces accelerating the convergence of credit and equity markets:

The rise of credit ETFs and the "ETF bid".

The electronification of credit trading and tighter bid-offer spreads.

The application of equity-style factors (value, momentum, quality) in credit selection.

The impact of central bank policy on both asset classes simultaneously.

We’ll explore how these forces are transforming the mechanics of credit, and how they’re changing the role credit plays in portfolios and markets.