Equity Vulnerability Scores: Q3 2025 Update

We update our scoring model to track how risk profiles have shifted across S&P 500 sectors and companies.

Three months after publishing our framework for assessing equity vulnerability across the S&P 500, we revisit our scoring model to track how risk profiles have shifted across sectors and companies.

The Energy and Real Estate sectors show elevated risk, based on a combination of low return performance, high P/E ratios, and high leverage.

Most of the companies we flagged three months ago remain high risk. However, a few have seen meaningful drops in their scores due to improved returns or deleveraging, including Microchip Technology, Warner Bros. Discovery, and CrowdStrike.

We highlight 15 new additions to our high-risk index. These companies exhibit a blend of weak momentum, high volatility, stretched valuations, and/or heavy debt loads.

Scoring S&P 500 Vulnerability

In a previous article, we introduced a simple but effective regression model to help identify the most vulnerable S&P 500 companies, i.e., those most at risk of sharp equity drawdowns in a recession.

The main drivers of the model are as follows:

Momentum: Strong recent returns are protective; lagging stocks are more vulnerable.

Volatility: Higher recent price volatility is associated with larger future drawdowns.

Valuation: Both very high and very low P/E ratios signal increased risk.

Leverage: Companies with higher debt relative to earnings experience deeper losses in downturns.

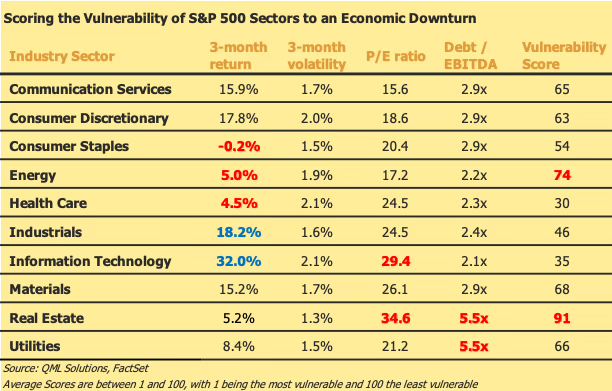

Applying the model across the S&P 500 (excluding financials), we assign each company a Vulnerability Score from 1 (least vulnerable) to 100 (most vulnerable).The table below shows the average score for each S&P 500 non-financial sector, along with the main drivers of the score.

The Energy and Real Estate sectors exhibit the highest scores, driven mainly by their relatively weak equity performance, while the Real Estate and Utilities sectors have the highest debt/EBITDA ratios. Overall, Real Estate has by far the highest score, and is likely the most exposed to an economic downturn. The Energy and Materials sectors also have relatively high average scores, indicating pockets of vulnerability in these sectors.

Updating Our Vulnerability Index

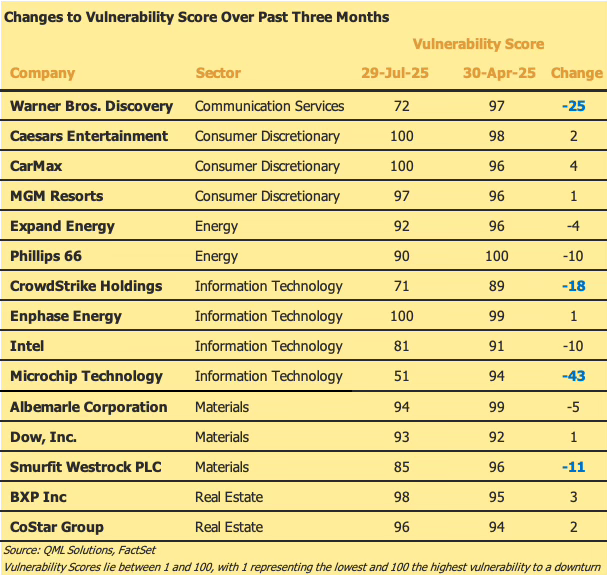

The table below contains the 15 S&P 500 companies that were highlighted in our previous article, and shows how their Vulnerability Scores have changed over past the three months.

While most companies remained within five points of the scores we assigned in April 2025, several companies moved out of the high risk category, i.e. scores below 85. The top movers were Microchip Technology, Warner Bros. Discovery, CrowdStrike and Smurfit Westrock. All four companies saw strong improvements in 3-month returns, while Warner Bros. Discovery and Smurfit Westrock also reduced debt to EBITDA by close to a turn.

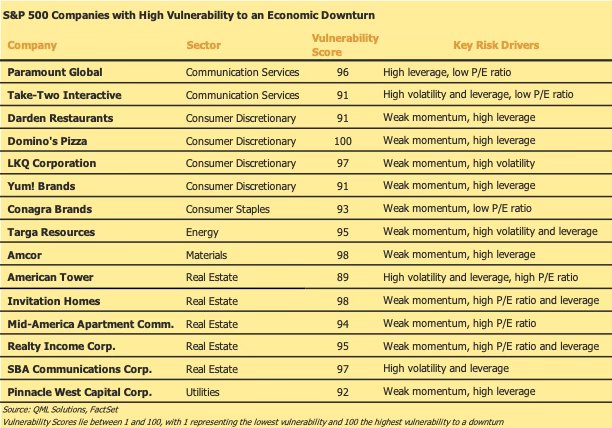

We highlight below 15 companies that are new additions to our index of high risk companies with scores above 85, i.e. the firms most at risk of significant drawdowns should macro conditions deteriorate. Each company exhibits a blend of poor return performance, high volatility, stretched valuations, and/or heavy debt loads. The full list of companies is available on request.

The content published by QML Solutions is for informational and educational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security or financial instrument. The views expressed are solely those of the authors and are subject to change without notice. While we strive for accuracy, we make no guarantees about the completeness or reliability of any information presented. Any investment decisions should be made in consultation with a qualified financial advisor and based on your own objectives, financial situation, and risk tolerance. QML Solutions and its authors disclaim any liability for any direct or consequential loss arising from reliance on the information provided.