Fallen Angels Part 1 – The BBB Companies Most at Risk of a Downgrade to High Yield

We screened over 300 BBB companies to find the firms most likely to fall to high yield in 2026 and 2027.

Annual downgrades of US BBB-rated companies to high yield (fallen angels) have increased in 2025 from cyclical lows, and will soon rise above the historical average.

To identify the firms most at risk of becoming fallen angels, we screened over 300 BBB issuers using a combination of factors, including high leverage, low interest coverage, refinancing risk and rating agency outlooks.

We highlight ten BBB companies that could fall to high yield in 2026/2027, with a combined index debt total of close to $200 bn.

Tight Spreads, Fragile Foundations

U.S. investment grade (IG) spreads are hovering near historic tights, with the ICE BofA US IG index trading around 80 bp, well below its historical median of 170 bp. But that apparent stability masks rising risks within the BBB tier, which currently stands at $4.2 trillion, or 45% of total US IG debt. Over 20% of BBB debt now sits one notch above high yield, and leverage metrics among the weakest BBB issuers have drifted higher even as interest coverage plateaus.

The recent collapse of Tricolor and First Brands has reignited concerns that market access can vanish quickly for highly leveraged credits once sentiment turns. In addition, these defaults have exposed weaknesses in the private credit market that could spill over to the banking sector, and ultimately to the wider economy. With over $150 bn of low-BBB debt due to mature in 2026/2027, a wave of downgrades — or even a modest re-pricing of credit risk — could test the limits of liquidity in what has become a tightly wound market.

The Fallen Angel Cycle

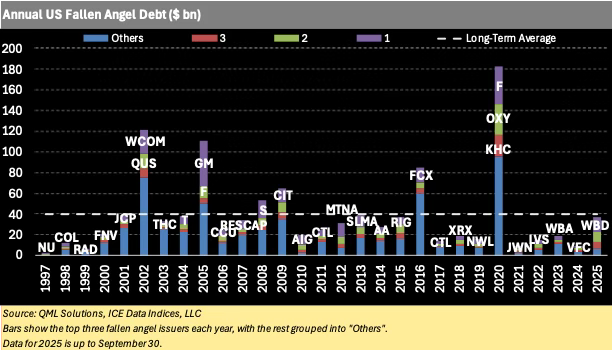

The chart below shows the face value of BBB debt in the ICE BofA US IG index that has been downgraded to high yield (HY) each year. Each bar shows the face value of the three largest fallen angel issuers, with the rest grouped as ”Others”. For example, in 2020 Ford (F) was the largest fallen angel, with $36 bn of debt downgraded to HY, followed by Occidental Petroleum (OXY) with $29 bn of fallen angel debt. 2020 was by far the worst year for fallen angels, with 224 bonds from 33 issuers downgraded to HY as the COVID pandemic intensified.

Between 2021 and 2024, US fallen angel debt remained well below the long-term average of $39 bn, with fewer than ten issuers downgraded to HY each year. However, so far this year we have seen $37 bn of fallen angel debt, $14 bn of which came from the downgrade of Warner Bros. Discovery (WBD) to HY in June 2025. The tally of fallen angel debt in 2025 is therefore likely to rise substantially above the long-term average.

Potential Fallen Angels in 2026/2027

We screened over 300 BBB issuers to find the companies most likely to be downgraded to HY over the next 12 to 24 months. Our screen includes the following criteria:

High Leverage – Net Debt to EBITDA greater than 4x.

Low Interest Coverage – EBITDA to Interest Expense below 6x.

Moderate to high refinancing risk.

Wide/volatile credit spreads.

Negative rating agency outlooks.

The table below contains 10 BBB issuers that met most – if not all – of the above criteria. Boeing (BA), CharterCommunications (CHTR) and CVS Health (CVS) are the largest issuers, with a combined total of $151 bn of index debt. (The $53.7 bn of CHTR debt is secured – its unsecured debt is already HY.) CVS is currently rated mid-BBB, and is therefore unlikely to fall to HY in 2026, but a downgrade to low-BBB next year, followed by another notch downgrade to HY in 2027, is a real possibility. Crown Castle (CCI) and Piedmont Operating LP (PDM) also stand out, with over 30% of index debt needing to be refinanced before the end of 2028.

In forthcoming articles in our series on Fallen Angels, we will focus on the dynamics of spreads and prices around the downgrade to high yield, in particular the impact of forced selling on fallen angel bond pricing. We will also study the lifecycle of fallen angels – how often fallen angels make the roundtrip back to investment grade, and the likelihood of a fallen angel ultimately defaulting.

The content published by QML Solutions is for informational and educational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security or financial instrument. The views expressed are solely those of the authors and are subject to change without notice. While we strive for accuracy, we make no guarantees about the completeness or reliability of any information presented. Any investment decisions should be made in consultation with a qualified financial advisor and based on your own objectives, financial situation, and risk tolerance. QML Solutions and its authors disclaim any liability for any direct or consequential loss arising from reliance on the information provided.