Credit-Equity Convergence Part 2: The ETF Bid

We quantify how ETF demand for investment grade corporate bonds impacts the liquidity and pricing of the underlying securities.

ETF ownership improves bond liquidity: Bonds held by large IG ETFs consistently trade with tighter bid-offer spreads, even after controlling for maturity, age, size, and yield.

The “ETF Bid” is measurable: A one standard deviation increase in ETF ownership is associated with a 4 bp reduction in bid-offer spreads — a meaningful liquidity premium.

ETF-owned bonds trade at a premium: Bonds more heavily owned by ETFs tend to have tighter option-adjusted spreads and higher prices, all else equal.

The growth of ETFs is pushing credit markets toward higher turnover, better execution, and greater price transparency, blurring the lines between debt and equity.

Introduction

In Part 1 of this series, we showed how credit and equity markets are becoming increasingly correlated. One of the drivers of this increased correlation is the growth of corporate bond ETFs, which are more liquid, price on an intraday basis, and are easier to short/hedge than the underlying cash bonds, features traditionally associated with equities. However, the impact of ETFs goes far deeper than this, as the ETF demand for corporate bonds has resulted in improvements in the liquidity and pricing of the underlying securities – the so-called “ETF Bid.” In this article, wequantify the ETF Bid by combining recent data on US IG bonds with the holdings of the largest IG ETFs.

The Explosive Growth of Corporate Bond ETFs

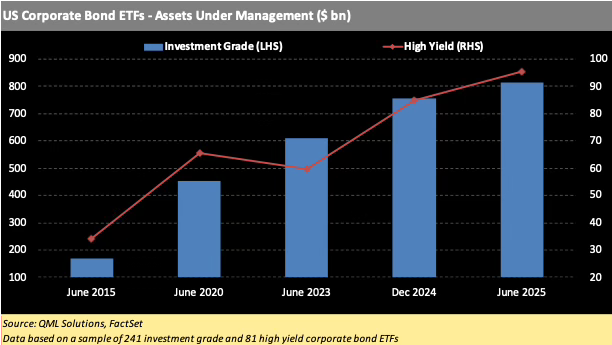

Over the past decade, corporate bond ETFs have gone from a niche product to a core vehicle for fixed income exposure, with assets under management (AUM) of US Investment Grade (IG) ETFs rising from under $200 bn in 2015 to over $800 bn in 2025. The AUM of US High Yield (HY) ETFs has nearly tripled, from $34 bn a decade ago to close to $100 bn today.

Persistent Inflows to Credit ETFs

Over the last year, the net flows to US corporate bond ETFs have been overwhelmingly positive. Investment Grade ETFs posted a net inflow of $47 bn so far this year, and close to $120 bn over the past 12 months.

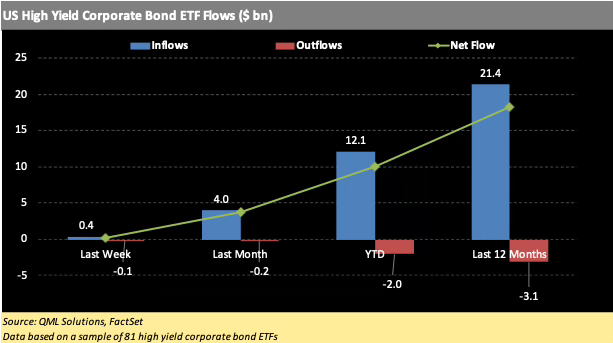

High Yield ETFs have also benefitted from solid inflows recently, with a net inflow of $10 bn since the beginning of the year, and just over $18 bn over the past 12 months.

These persistent inflows have created a systematic bid for certain types of bonds — and that bid has measurable effects.

Quantifying the ETF Bid – Liquidity

Our analysis focused on investment grade (IG) corporate bonds, and combined recent pricing data from ICE Data Indices, LLC with information on the holdings of ten of the largest IG corporate bond ETFs.

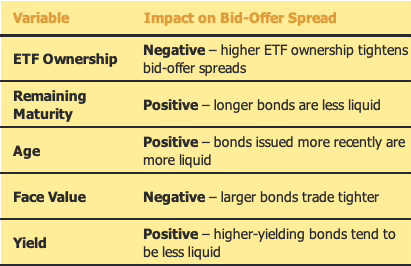

To test the relationship between ETF ownership and liquidity, we regressed each bond’s bid-offer spread on:

ETF ownership (% of face value held by our sample of IG ETFs)

Remaining maturity

Age (years since issuance)

Face value

Yield

Our regression equation is

All of the five variables were statistically significant at a 99% confidence level, and their relationship with bid-offer spreads followed the expected pattern:

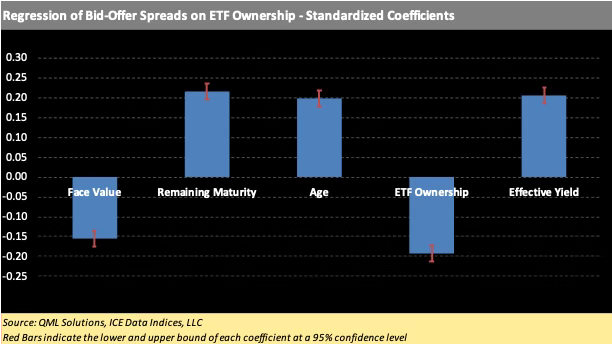

As shown in the chart below, four of the five variables have a broadly similar impact on a bond’s liquidity profile, and face value has a slightly lower impact. Our regression data show that an increase of one standard deviation in ETF ownership (2% of a bond’s face value) is associated with a tightening of approximately 4 bp in the bid-offer spread.

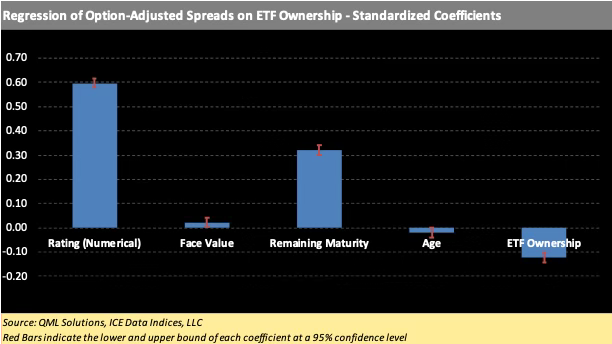

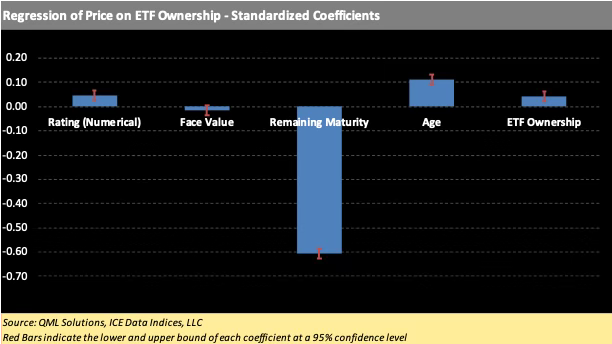

ETF Ownership Also Affects Pricing

We ran a second set of regressions to examine how ETF ownership affects bond spreads and prices. We replaced the yield with the rating of the bond as a number between 1 and 10 (AAA = 1, AA1 = 2, etc.).

Option-Adjusted Spread (OAS) Regression:

Bond rating had the strongest influence (as expected).

Remaining maturity also had a large impact — longer bonds trade with wider spreads.

ETF ownership was statistically significant and negative, confirming that bonds held by more ETFs tend to trade at tighter spreads, all else equal.

Price Regression:

Remaining maturity had a large negative impact on price — reflecting rate sensitivity.

ETF ownership showed a positive and significant relationship with price — suggesting that ETF-held bonds trade at a premium.

This analysis confirms what many traders and PMs have long observed: ETF ownership not only increases a bond’s liquidity but also enhances its valuation. As ETFs continue to grow, these dynamics will only strengthen.

The content published by QML Solutions is for informational and educational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security or financial instrument. The views expressed are solely those of the authors and are subject to change without notice. While we strive for accuracy, we make no guarantees about the completeness or reliability of any information presented.Any investment decisions should be made in consultation with a qualified financial advisor and based on your own objectives, financial situation, and risk tolerance. QML Solutions and its authors disclaim any liability for any direct or consequential loss arising from reliance on the information provided.